Covid-19: Legislative Response for Tax – Darkness before Dawn

The rapidly evolving crisis has meant the government and opposition in the spirit of bipartisanship have enacted a number of measures. These measures include the below listed bills:

- Coronavirus Economic Response Package Omnibus Bill 2020

- Guarantee of Lending to Small and Medium Enterprises (Coronavirus Economic Response Package) Bill 2020

- Australian Business Growth Fund (Coronavirus Economic Response Package) Bill 2020

- Assistance for Severely Affected Regions (Special Appropriation) (Coronavirus Economic Response Package) Bill 2020

- Structured Finance Support (Coronavirus Economic Response Package) Bill 2020

- Appropriation (Coronavirus Economic Response Package) Bill (No. 1) 2019-2020

- Appropriation (Coronavirus Economic Response Package) Bill (No. 2) 2019-2020

- Boosting Cash Flow for Employers (Coronavirus Economic Response Package) Bill 2020

This update will, consistent with the firm’s previous update, focus on the small and medium sized business tax measures. The aim of this release will be to provide the legislatively enshrined eligibility criteria to claim concessions and the mechanics of how to go about making a claim. This should assist businesses in having the certainty to plan for their future. If any professional advisor is seeking to utilise these measures and would like assistance please reach out.

Boosting cash flow for employers

The key measure for employees is the boosting cash flow measure tied to an employer’s liability to pay PAYG withholding for their employees. Our previous update made it clear that two types of cash flow payments or credits would be made that were tied to an employer’s Business Activity Statement. These were as follows:

- Cash Flow Boost in the 2020 Financial Year (“First Cash Flow Boost Payment”)

- Cash Flow Boost in the 2021 Financial Year (“Second Cash Flow Boost Payment”)

The announcement has largely been enacted, however further detail on eligibility of this measure is contained in this update.

First Cash Flow Boost Payment – Eligibility for NFP & Business

The payments will generally be made on lodgement of the activity statement notifying the Commissioner of their withholding liabilities for the period and can be provided as a credit against tax liabilities. The payments are available to all small to medium sized business and not-for-profit entities that make eligible payments, including individuals that carry on a business as a sole trader, partnerships and trusts provided they satisfy the other eligibility requirements. Eligible payments include salary and wages, but can also include director’s fees and payments to contractors that are subject to voluntary withholding arrangements.

The first cash flow boost is payable by the Commissioner in relation to periods ending from March 2020 to June 2020. Entities are eligible to receive the payment for a period where they meet conditions for all entities and where the entity is a business (rather than a not for profit) meets additional criteria.

Eligibility – Small to Medium Sized Business

The conditions that all entities must meet are as follows:

- The entities are small to medium sized businesses or the Commissioner reasonably believes them to be so. This test has two alternative limbs. To provide context an entity is a small to medium size if:

- Carry on a business (not for profits are taken to meet this condition); and

- Have aggregated turnover under $50 million.

The two alternative limbs of the test are as follows:

- the entity was a small or medium business entity, or a charity or other not-for-profit entity of equivalent size, for the 2019 income year of the entity for which an assessment of income tax has been made by the Commissioner; or

the Commissioner is reasonably satisfied that it is likely that the entity is a small or medium business entity, or a charity or other not-for-profit entity of equivalent size, for the income year that includes the period;

Eligibility – Other Criteria for All Entities

- The entity makes a payment that is subject to withholding obligations under Subdivisions 12-B, 12-C or 12-D of schedule 1 to the Taxation Administration Act 1953 (Cth) (broadly, a payment of wages or salary or similar remuneration), whether or not any amount is actually withheld, in the period;

- the entity has notified the Commissioner of their entitlement in the approved form;

- the period is one of the following:

- the quarters ending in March 2020 or June 2020; and

- the months of March 2020, April 2020, May 2020 or June 2020;

- The entity (or an associate or agent of an entity) has not engaged in a scheme for the sole or dominant purpose of seeking to make the entity entitled to the first cash flow boost or increase the entitlement of the entity to the first cash flow boost.

Eligibility – Businesses Only (Excludes NFP)

- Where the entity is not an Australian Charities and Not-for-profits Commission registered charity, it must meet all of the following conditions:

- Held an ABN on 12 March 2020; and

- The entity met either of the following conditions:

- Derived assessable income from carrying on a business in the 2018-19 income year, or

- Made one or more supplies for consideration in the course of an enterprise it carried on within Australia in both the following circumstances:

- In tax periods commencing after 1 July 2018 and ending before 12 March 2020; and

- Notice of the income or supplies was held by the Commissioner on or before 12 March 2020 or within such further time as the Commissioner allows.

The Cash Flow Boost Bill also provides for the Commissioner to make second cash flow boost payments upon lodgement of the activity statements for eligible periods from June to September 2020 to entities that were entitled to the first cash flow boost.

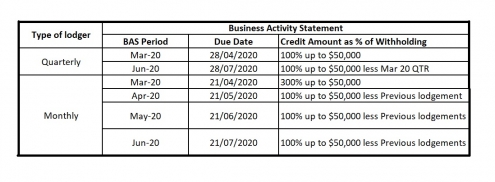

Calculation of First Cash Flow Boost Payment

All eligible entities will receive a minimum cash flow boost payment of $10,000 in the first period for which they are eligible. Entities will receive further amounts, based on the amount withheld, up to a maximum total of $50,000 across all cash flow bonus payments to the entity.

If the minimum amount and maximum cap do not apply, the amount of the first cash flow boost payment is equal to 100 per cent of the amount that has been withheld for Quarterly withholding entities.

However, if the payment is for the month of March 2020, the entity is entitled to a payment of an amount equal to 300 per cent of the amount that has been withheld. This can be represented diagrammatically as follows:

Calculation of Second Cash Flow Boost Payment

The Commissioner must also make the second cash flow boost payments to an entity for a total amount equal to the amount of the first cash flow boost payment/(s) to which the entity is entitled.

These second cash flow boost payments are payable in equal instalments for either:

- the months of June, July, August and September 2020; or

- the June and September 2020 quarters.

The second cash flow boost payments will generally be made on lodgement of the activity statement containing the GST return of the entity for the period.

For monthly activity statement lodgers, the additional payments will be delivered as an automatic credit in the activity statement system. This will be equal to a quarter of their total initial First Boosting Cash Flow payment for Employers payment following the lodgment of their June 2020, July 2020, August 2020 and September 2020 activity statements (up to a total of $50,000).

For quarterly activity statement lodgers the additional payments will be delivered as an automatic credit in the activity statement system. This will be equal to half of their total initial First Boosting Cash Flow payment for Employers payment following the lodgment of their June 2020 and September 2020 activity statements (up to a total of $50,000).

Instant Asset Write Off and Accelerated Depreciation

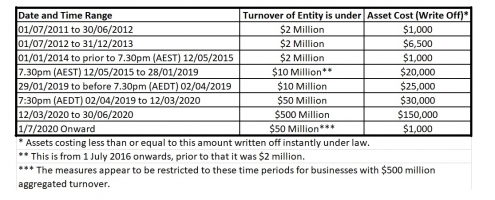

The first depreciation measure increases the instant asset write off from $30,000 to $150,000 for the period 12 March 2020 to 30 June 2020. This measure is open to business entities with aggregate turnover of up to $500 million to access this concession.

The second depreciation measure applies for the period 12 March 2020 to 30 June 2021 where an asset is acquired and installed ready for use within this time period. This measure is also open to business entities with aggregate turnover of up to $500 million to access this concession. There are a number of exceptions that apply, most notably second hand assets.

Summary of Instant Asset Write Off Concession due to Covid-19 Measures

These measures and their rate and eligibility for instant asset write off purposes are best summarised in a table. This table is as follows:

Eligible small businesses must place assets which cannot be immediately deducted into the small business simplified depreciation pool and generally depreciate those assets at 15 percent in the first income year and 30 per cent each income year thereafter. The pool balance can also be immediately deducted if it is less than the applicable instant asset write-off threshold at the end of the income year (including existing pools).

Please note that assets acquired after 12 May 2015 by a small business with aggregated turnover under $10 million installed ready for use after 12 March 2020 but before 30 June 2020 will also be eligible to claim the $150,000 instant asset write off. This is in addition to the claims made under the included table. Any other entity that doesn’t meet this small business definition will need to both acquire and have installed ready for use assets between 12 March 2020 and 30 June 2020 to claim the $150,000 write off.

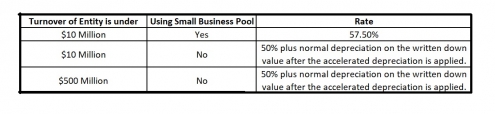

Summary of Accelerated Depreciation Concession due to Covid-19 Measures

The accelerated depreciation rate for eligible entities is one of three rates as follows:

The 50% above refers to the cost of the asset eligible for depreciation under Division 40 of the Income Tax Assessment Act 1997 (Cth). The accelerated depreciation deduction applies in one income year only, being the income year that the assets are first used or installed ready for use for a taxable purpose. This measure does not apply to assets that have been written off under the instant asset write off.

Assets Eligibility for claim (“Qualifying Asset”)

The assets able to be claimed must meet the following criteria generally:

- They must be ‘new’ assets that have not been previously held (and used or installed ready for use) by another entity (other than as trading stock or for testing and trialling purposes);

- The assets must be ones for which an entity has not claimed depreciation deductions, including under the instant asset write-off rules; and

- The assets first be held, and used or installed ready for use for a taxable purpose between 12 March 2020 and 30 June 2021 (inclusive).

However, some exceptions to be a qualifying asset apply. These exclusions include:

- a commitment to the asset was entered into before 12 March 2020;

- the asset is a second hand asset;

- Division 40 of the Income Tax Assessment Act 1997 (Cth) does not apply to the asset; or

- the asset would not be in Australia.

These conditions will circumvent the qualifying nature of the asset.

Entity Eligibility for claim

The entity able to claim must meet the following criteria generally:

- the income year is the year that the entity starts to use the asset, or has it installed ready for use for a taxable purpose;

- the entity has aggregated turnover of less than $500 million for the income year; and

- the asset is a qualifying asset.

Once these criteria and those of the qualifying asset are met, a claim may be available subject to exceptions.

Other General Exceptions to Eligibility

An entity is not eligible to claim the accelerated depreciation deductions if the decline in value of the asset has already been deducted under the instant asset write-off rules in section 40-82 of the Income Tax Assessment Act 1997 (Cth).

Similarly, an entity is not eligible to apply the accelerated depreciation deductions if the decline in value of the asset is worked out under:

- Subdivision 40-E of the Income Tax Assessment Act 1997 (Cth), regarding low-value and software development pools; or

- Subdivision 40-F of the Income Tax Assessment Act 1997 (Cth), regarding certain primary production depreciating assets (such as water facilities, horticultural plants, fodder storage assets and fencing assets).

Capital allowance arrangements described in Subdivisions 40-E to 40-K of the Income Tax Assessment Act 1997 (Cth) are not eligible for decline in value to be worked out under these amendments. Most of these arrangements either apply to pooled amounts, do not involve an asset or result in an immediate write-off of expenditure.

Summary

These measures are key stimulus measures from the Tax Office. The measures are increasingly difficult to plan for given the date is now 24 March 2020. VT Advisory wants to ensure the legislatively binding measures are published as soon as possible to allow all parties to seek guidance and obtain relevant concessions.

The Covid-19 crisis will get worse for all our clients and the entire business community. We understand this community is made up of people. We recall the GFC and its impact. Our guidance is that you all be kind to one and other. That and you keep in mind that it is always darkest before the dawn.